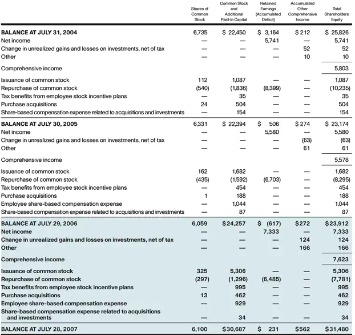

At first look, commitments on the company’s balance sheet add to its total risk. Items included on a company’s balance sheet are known as “on-balance sheet items,” Items that are “off-balance sheets” are not disclosed on a company’s balance sheet. Conversely, operating leases moving onto the balance sheet under IFRS 16 will impact both EBITDA and the D/E ratio. If the company decides to take a loan, it would lead to a debt-to-equity ratio that will look extremely off to its investors.

These items can still be disclosed in the notes given in the financial statements. The use of off-balance sheet financing can potentially be used to mislead investors, financial institutions, and other financing entities to believe that the company is in a better financial position than they actually are. Off-balance sheet items, also referred to as incognito leverage means that the company itself does not have a direct claim to the assets so it does not record them on the balance sheet. The monthly rental expense will be shown in the income statement and the company would have successfully kept this asset, or a possible liability if they had borrowed the funds, off the balance sheet. Almost all companies have this asset category and the default risk of this asset is the highest.

Lease liabilities on the balance sheet: Measuring the impact

Off-balance-sheet financing refers to types of transactions and methods of accounting for transactions in which no liabilities are recorded to an organization’s financial statements. The financial obligations that result from OBSF are known as off-balance-sheet liabilities. In many cases, off-balance-sheet liabilities are simply recorded as operating expenses. The company is able to do so by transferring the ownership of certain assets to other parties or by engaging in transactions that will allow them to not be reported in the financial statements under different accounting standards. An example of real life situation is a firm seeking to raise a loan, and its lender set a condition that its debt-to-equity ratio shall not be allowed to increase over the loan term.

To learn more about why the lease accounting standards were changed, the new challenges in accounting for leases, as well as the financial and balance-sheet impact of these changes, check out the following articles. Under ASC 842, there is a single, straight-line lease expense for operating leases recorded in operating income, similar to the rent or operating expense previously recorded. This means there is no significant change to the income statement when compared to ASC 840. In addition to the large equipment purchase mentioned above, there are other way and reasons to employ off-balance sheet financing. A company could create a separate entity (sometimes known as a SPE – Special Purpose Entity), purchase the equipment through the new entity, and then lease it back to the original company.

In this case, the company can receive the item they need without raising it’s debt burden, allowing the company to use it’s borrowing funds for something else. The Federal Reserve, the central bank of the United States, provides the nation with a safe, flexible, and stable monetary and financial system. We have taken a closer look at the financial needs of our customers and developed our modules and apps for your Odoo system. Designed for freelancers and small business owners, Debitoor invoicing software makes it quick and easy to issue professional invoices and manage your business finances. OBS exposures, for instance, frequently appear after rights have been assigned or responsibilities have been resolved from an accounting and legal standpoint. Adam Hayes, Ph.D., CFA, is a financial writer with 15+ years Wall Street experience as a derivatives trader.

Are banks dead? Or are the reports greatly exaggerated?

OBS activities can be accomplished through setting up a SPE (Special Purpose Entity) to purchase equipment and lease it back to the original company. Companies can also use debt factoring, letters of credit from a bank, and joint ventures as part of OBS acitivities. Sometimes this occurs because the Generally Accepted Accounting Principles (GAAP) don’t require the disclosure. The implementation of ASC 842 greatly narrows what can be properly left off the balance sheet.

- The liability was calculated as the present value of the minimum lease payments over the lease term and the interest portion of the lease payments was categorized as interest expense.

- These items are assets and liabilities of the company, even if they don’t show up on the balance sheet.

- Using OBS activities may improve earnings ratios like the asset turnover ratio.

- The comprehensive features and extensions we have developed, in addition to the Odoo standard, will simplify your processes and allow you to manage factoring with your partner.

It took action after establishing that public companies in the United States with operating leases carried over $1 trillion in OBSF for leasing obligations. According to its findings, about 85% of leases were not reported on balance sheets, making it difficult for investors to determine companies’ leasing activities and ability to repay their debts. It stands for off balance sheet; all items (assets and liabilities) that are not reported on the statement of financial position (balance sheet) of an entity. Typically, these items are classified off balance sheet because an entity has no control over them- that is, it is not the legal owner of such items. In financial reporting, these items are shown in the notes to financial statements (footnotes).

Journal of Banking & Finance

For example, when loans are securitized and sold off as investments, the secured debt is often kept off the bank’s books. Prior to a change in accounting rules that brought obligations relating to most significant operating leases onto the balance sheet, an operating lease was one of the most common off-balance items. For example, our recent study, the Lease Liabilities Index Report, demonstrates how common these transactions were. Among a sample of over 400 businesses that transitioned to the new lease accounting standards, the recognition of previously-excluded leases to balance sheets led to an average increase of 1,479% in lease lease liabilities. The study includes an analysis of these businesses’ balance sheets, both pre- and post-transition, to highlight the impact of transitioning to the new rules. Since an operating lease payment was simply an operating expense under the old lease accounting standards, the lease obligation was not included in total liabilities.

- Yet, they could be used to deceive other stakeholders, such as investors or other financial institutions.

- The company itself has no direct claim to the assets, so it does not record them on its balance sheet (they are off-balance-sheet assets), while it usually has some basic fiduciary duties with respect to the client.

- The numerator (debt) will increase while Shareholder’s Equity will not be significantly impacted (as addressed above).

- Because of the new lease accounting standard, the only type of operating lease allowed to be an off–balance-sheet lease is an operating lease with a term that is less than 12 months duration.

- Designed for freelancers and small business owners, Debitoor invoicing software makes it quick and easy to issue professional invoices and manage your business finances.

Collecting debts is also time consuming, so factoring can also lead to staff reduction and savings in personnel costs. The factoring company also assumes the risk of bad debt – if they can’t collect what’s owed, they’re the ones out the money. Access financial statement examples for before and after the new lease standard. Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling. Investors will benefit from having a better grasp of OBS if they want to know how much a company has offset on its balance sheet.

Recording capital leases on the balance sheet under ASC 840

For example, financial institutions often offer asset management or brokerage services to their clients. The assets managed or brokered as part of these offered services (often securities) usually belong to the individual clients directly or in trust, although the company provides management, depository or other services to the client. The company itself has no direct claim to the assets, so it does not record them on its balance sheet (they are off-balance-sheet assets), while it usually has some basic fiduciary duties with respect to the client. Financial institutions may report off-balance-sheet items in their accounting statements formally, and may also refer to “assets under management”, a figure that may include on- and off-balance-sheet items.

Average Prices Up on Day 1 of OBS June – BloodHorse.com

Average Prices Up on Day 1 of OBS June.

Posted: Tue, 13 Jun 2023 07:00:00 GMT [source]

The indirect financial reporting of the related liabilities within the notes to the financial statements – or possibly not at all – rather than directly on the face of the balance sheet. To help perform a detailed lease vs. buy analysis, we have created the LeaseQuery Lease vs. Buy Calculator. This robust calculator will help your organization make an informed decision, based on updated considerations from the new accounting standards, on whether to lease or purchase its next asset. ASC 842, IFRS 16, and GASB 87 allow for the practical exception of leases that are considered short term. This results in a population of leases under each standard continuing to be recorded consistent with the legacy standards, or continuing to utilize an OBS approach.

Does non-interest income make banks more risky? Retail- versus investment-oriented banks

It does so by engaging in transactions that are designed to shift the legal ownership of certain transactions to other entities. Or, the transactions are designed to sidestep the reporting requirements of the applicable accounting framework, such as GAAP or IFRS. Going forward, companies that are incentivized on EBITDA may begin to choose finance leases over operating leases as a way to benefit from this change.

Prevent Blindness provides educational resources and information … – Ophthalmology Times

Prevent Blindness provides educational resources and information ….

Posted: Thu, 01 Jun 2023 07:00:00 GMT [source]

Though off balance sheet assets and liabilities do not appear on the balance sheet, they may still be noted within the accompanying financial statement footnotes. Companies use this method of accounting to lessen the impact of ownership of certain assets and obligations of certain liabilities on their financial statements. The company keeps certain items off of its balance sheet to present a stronger balance sheet to the investors.

Accounting You Can Count On

Off-balance sheet (OBS) items is a term for assets or liabilities that do not appear on a company’s balance sheet. Although not recorded on the balance sheet, they are still assets and liabilities of the company. Off-balance sheet items are typically those not owned by or are a direct obligation of the company.

Going forward, one major factor in this decision will be how lease classification impacts various metrics used in financial statement analysis. Previously, off-balance-sheet operating leases could be used to affect these types of metrics. This prepaid insurance complete guide on prepaid insurance has changed in several ways and, furthermore, there are significant differences between the FASB and IFRS standards. In short, capital leases, which are now classified as finance leases under ASC 842, were treated like financed purchases.

Nedavni komentarji